‘The dangers of life are infinite, and among them is safety’ – Goethe.

The Securities and Exchange Board of India (SEBI) issued a discussion paper on the ‘mandatory safety net mechanism’ in September 2012 (the SEBI discussion paper), inviting public comments. Briefly, this contemplates a mechanism wherein, in the event of a fall in share price within a specified period subsequent to listing, retail investors are able to tender back their shares purchased in an initial public offering (IPO), at the issue price, to the designated safety net provider.

The stated rationale of the proposal to mandate that all IPOs shall provide for a safety net mechanism is to reinforce retail confidence in the Indian capital markets and discipline issuers and intermediaries on fair pricing of IPOs. The SEBI discussion paper observes that, of 117 companies listed in India during 2008 to 2011, stocks of 72 companies (ie 62%) were trading below issue price after six months of listing, of which stocks of 55 companies witnessed a fall of over 20% of the issue price.

The genesis of SEBI’s protective stance towards the retail investor goes back much further. SEBI has prescribed a plethora of measures aimed at protecting investors, ranging from comprehensive disclosure requirements prescribed for offer documents in public issues (including disclosure on the justification for the basis for the issue price), to, more recently, a circular in September 2011 on disclosure of price information of past issues handled by investment banks and a circular in January 2012 on disclosure of track record of public issues managed by investment banks, which would enable an informed investment decision. In addition, the amendment to the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (the ICDR Regulations) in October 2012 required, firstly, at least 75% participation by sophisticated investors, ie, qualified institutional buyers (QIBs) in public issues of companies that do not satisfy stipulated financial criteria (an increase over the existing requirement for 50% QIB participation for such companies) and, secondly, mandatory allotment of the minimum bid lot to retail investors in a public issue, subject to availability of shares.

Regulation 44 of the ICDR Regulations already provides that an issuer may provide a safety net for securities offered in any public issue (in consultation with the investment banks), provided that such arrangement provides for an offer to purchase up to 1,000 specified securities per original resident retail individual allottee at the issue price, within six months of allotment. The SEBI discussion paper goes further, contemplating a mandatory safety net for resident retail individual investors who have made applications in an IPO not exceeding 50,000 rupees, triggered by a 20% fall in share price over and above general fall (if any) in the specified market index. Under the SEBI discussion paper, the primary safety net obligation rests with the promoters of the issuer, who may fulfil this obligation directly or through merchant bankers or any other safety net provider.

The market has had a mixed reaction to the SEBI discussion paper. While small investors find comfort in the face of fears of reckless valuation and volatile stocks, market participants, such as investment banks, voice the apprehension that the SEBI discussion paper does not address the crisis of confidence that it seeks to resolve and instead opens a Pandora’s box of concerns, having the counterproductive effect of discouraging companies and promoters from accessing the Indian primary market (who may then choose to access equity markets in foreign jurisdictions).

Risk is an inherent characteristic of equity investment, which is why equity capital is also referred to as ‘risk capital’ (as distinguished from investment in debt, which carries assured returns). The SEBI discussion paper seeks to eliminate this element of the investment decision on the part of a retail investor by introducing a ‘money-back guarantee’ on equity shares, thereby altering the very nature of the instrument.

It is understood that a retail investor may lack the information or sophistication necessary to make a prudent investment (perhaps partly due to the sheer volume of disclosure contained in the typical IPO offer document). However, a safety net would not help to educate investors or develop sophistication in a nascent market. Moreover, while it is possible that a post-listing price crash may be due to improper valuation, which could have been pre-empted by proper due diligence by the investment banks, there may be other factors at play (particularly in heavily regulated sectors such as power, telecom and the financial sector, where amendments to law and policy are frequently notified) that are unforeseeable at the time of due diligence and valuation. The safety net being triggered by a 20% fall in share price over and above general fall in the specified market index may be a somewhat insufficient methodology, applied in a vacuum (devoid of industry and company-specific factors that may be more relevant to post-listing price fall). Moreover, a six-month period may be inadequate to judge whether price discovery was flawed.

‘Nobody wants to fall into a safety net, because it means the structure in which they’ve been living is in a state of collapse and they have no choice but to tumble downwards. However, it beats the alternative’ – Lemony Snicket, on Occupy Wall Street.

While the mandatory safety net mechanism has not yet been notified by SEBI, Sai Silks (Kalamandir) Ltd voluntarily offered a safety net in its proposed 890m rupee IPO in January 2013, offering resident retail individual investors the opportunity to tender back their shares at any time within six months from the date of allotment in the event of any fall in share price below the issue price. The company structured its issue to offer 55% to retail investors (where the minimum requirement was only 35% retail allocation). While the sizeable retail portion was 1.31 times subscribed (indicating an enthusiastic response from retail investors to the safety net), the complete lack of QIB participation and only 43% subscription by non-institutional investors caused the company to withdraw its IPO. Therefore, while the implementation of the safety net was not tested in this IPO, the lesson learned here is that the safety net, while it may encourage retail participation, is not sufficient to ensure the success of public issues or to revitalise the market.

A glance at securities laws of developed markets like the US, Japan, the UK and other European markets indicates that no mature market has a true equivalent of the safety net mechanism. The regulation of these markets rests primarily on enhanced disclosure norms and stringent enforcement, including through continuing post-listing disclosure and an evolving body of administrative and judicial precedent where instances of negligence or transgression such as inadequate due diligence, reckless valuation or price rigging would be strictly penalised.

‘All games have morals; and the game of Snakes and Ladders captures, as no other activity can hope to do, the eternal truth that for every ladder you climb, a snake is waiting just around the corner; and for every snake, a ladder will compensate… but I found, very early in my life, that the game lacked one crucial dimension, that of ambiguity – because, as events are about to show, it is also possible to slither down a ladder and climb to triumph on the venom of a snake…’ – Salman Rushdie, Midnight’s Children.

While it remains to be seen whether, when or in what form the mandatory safety net is implemented, there is cause for concern that, if the safety net is triggered for reasons beyond the investment banks’ reasonable control or foresight, the investment banks may nevertheless face regulatory action as well as reputational damage. Moreover, as this mechanism does not provide checks against the vagaries of the secondary market or instances of abuse (such as market manipulation and price rigging), it may provide small investors with nothing more than a false sense of security.

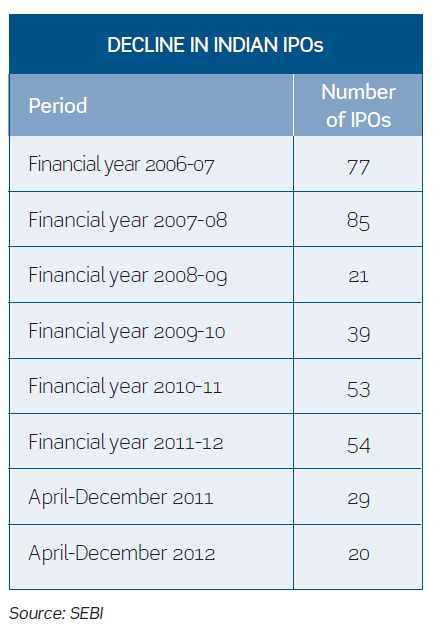

In addition, the market itself may stand to suffer collateral damage. The table above left illustrates the recent declining trend in Indian IPOs.

As is evident from these figures, one must bear in mind that we are yet to recover fully from the recent global economic slowdown. Therefore, today, it is more important than ever to facilitate Indian issuers and intermediaries to access the primary market. The mandatory safety net may create a further entry barrier for Indian companies seeking to access the anaemic Indian equity capital market, in which case SEBI’s aim of mobilising household savings and stabilising the market may remain largely unfulfilled. In fact, what may be more helpful is to focus on developing the largely untapped Indian debt capital market to offer retail investors a safer avenue for their investment.

In conclusion, while the one-size-fits-all approach of a mandatory safety net may be myopic (although well intentioned), the current provision for an optional safety net under Regulation 44 of the ICDR Regulations is sufficient. SEBI has already instituted welcome reforms aimed at better dissemination of information on price discovery and post-listing market performance as well as continuing disclosure for listed companies. Improved monitoring and enforcement will create depth, stability and integrity in the Indian primary and secondary markets and thus achieve the objective of mitigating risk for small investors.

By Prashant Gupta, partner, Monal Mukherjee, principal associate designate, and Manjari Tyagi, senior associate, Amarchand Mangaldas.

E-mail: prashant.gupta@amarchand.com; monal.mukherjee@amarchand.com; manjari.tyagi@amarchand.com.